Is Gold a Smart Hedge, or Just Shiny…. Should Gold be in Your Portfolio?

By Devon Walsh, CFA

Is it all glitter?

Due to geopolitical uncertainty, investments in rare metals like gold and silver have become a hot topic. Whether it’s your coworker mentioning gold ETFs, a family member insisting you buy coins, or headlines about foreign central banks hoarding bullion, the shiny metal seems to be everywhere. So, let’s discuss the pros and cons of holding gold, what your realistic expectations for its performance should be, and our stance on this attention-grabbing commodity.

Arguments for holding gold

Gold has been a store of value for thousands of years, long before paper money existed. Investors today still treat it as such, and gold has historically outperformed during periods of uncertainty. For example, during the 2008 financial crisis, gold climbed roughly 30% while the market fell by about 50%. At the start of 2020, when COVID fears sent the market down 30%, gold declined by only 2%. Because gold’s performance is generally uncorrelated with stock returns, it is viewed as a portfolio diversifier and a hedge against market volatility.

Gold also benefits from industrial usage, particularly due to its conductivity. The most sophisticated data center processers contain up to three times the gold used in pre-AI designs. According to the World Gold Council, technological demand, which accounts for 5% of gold’s total demand, rose 7% year over year in 2024 as more AI‑related hardware was manufactured. However, when gold prices rise sharply, manufacturers frequently look for more cost‑effective metal substitutes with similar conductive properties. As a result, AI-related use may create only temporary tailwinds for gold demand.

The other side of the coin

How does one value gold? It’s an age‑old question—and nearly impossible to answer without saying, “Find out what someone else is willing to pay for it.” Bonds pay interest, and companies return cash to shareholders through dividends, but gold does neither. Unless you choose to wear it or use it in manufacturing, gold simply sits in a vault, generating no cash flow. As Warren Buffett famously said during a speech at Harvard, “Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again, and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

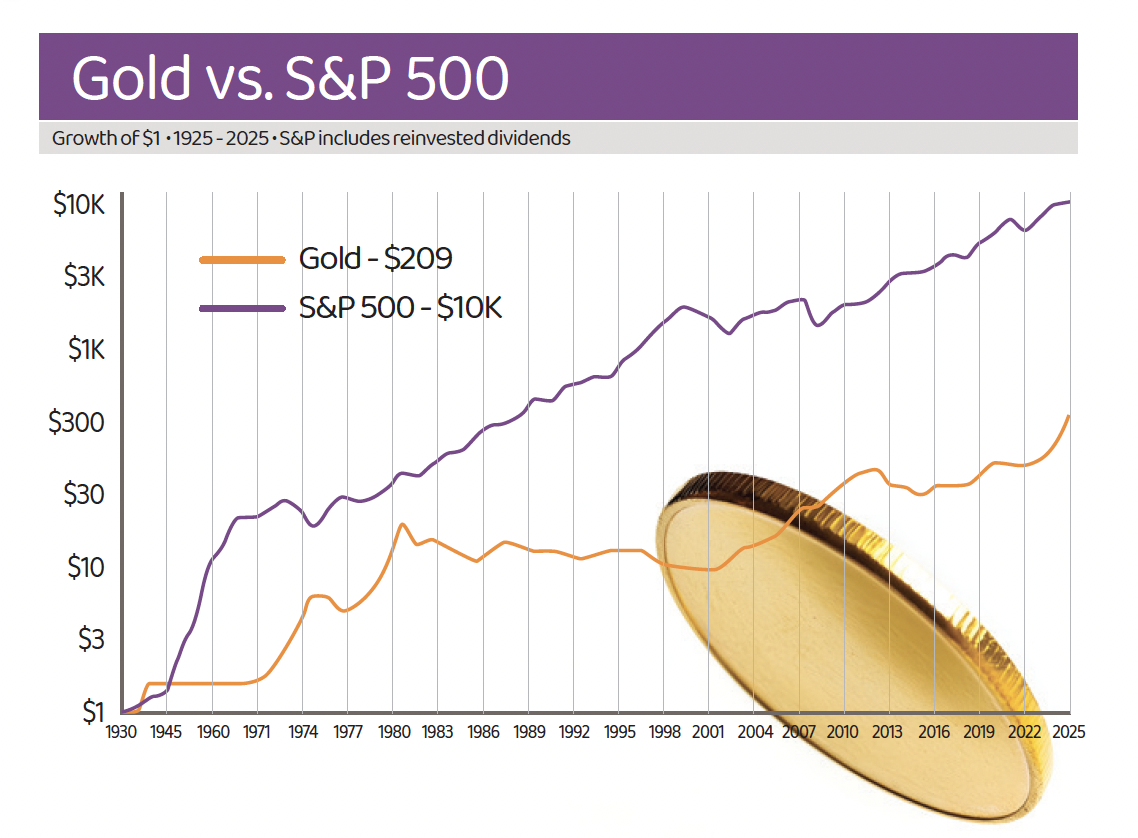

Because gold is often used as an inflation hedge, one might expect its price to rise steadily at roughly the rate of inflation. But historically, that hasn’t been the case. Gold tends to move in cycles—often sharp, emotionally driven ones—rather than smooth, predictable increases. Between 1970 and 1980, it surged eighteenfold as stagflation gripped the global economy. But what followed was a 20‑year period of declining prices, and gold didn’t surpass its 1980 peak of over $800 until 2007. The chart below compares performance of the S&P 500 to gold over the past century. Investing $1 in gold in 1925 would have resulted in $209 (5.5% annual return) at the end of 2025 while investing $1 in the S&P 500 would have resulted in $10,000 (9.5% annual return) at the end of 2025. As you can see, while equities seemed to mostly appreciate during the past century with times of decline corresponding to economic downturns, the price of gold moved in cycles with sharp upticks followed by sharp and then gradual declines over long periods of time.

History may be repeating today. Gold has seen a massive spike since early 2023, driven by geopolitical uncertainty. Should that uncertainty ease—for example, due to changes in expectations or monetary and fiscal policy—gold could fall just as dramatically as it has in past cycles. We received a preview of this dynamic when news broke about Donald Trump’s nominee for Federal Reserve chair, Kevin Warsh: gold fell 18% in a single day as markets reassessed future inflation expectations under a potentially hawkish chair.

Lastly, gold now faces more competition for investors focused on inflation hedging assets due to the rise in popularity of cryptocurrency. While crypto is still very speculative, it may replace gold as the inflation hedge in a portfolio in a future where consumers can buy and sell goods using different digital coins. If gold’s value is mainly derived from hedging inflation and another asset can hedge inflation and have actual transactional value, investors may reassess their gold holdings.

Do we believe in gold?

While a small weighting (5%) of gold in a portfolio may be useful for diversification, we believe that a sufficiently diverse portfolio can be achieved without it. Instead, we would rather own a portfolio with names that can be valued on their individual merit. As mentioned earlier, unlike fixed income instruments and publicly traded companies, we cannot value gold on a certain metric. Because of this, we cannot value gold on a fundamental basis and believe that there are other diversifying stocks and bonds that can take its place in a portfolio. On the stock side, companies with strong pricing power can continue to raise prices during highly inflationary periods. On the bond side, TIPS, or Treasury Inflation Protected Securities, pay a floating rate determined by CPI. If inflation were to increase, your rate of return on holding the bond would increase in tandem. These assets can be valued by future cashflows and are, therefore, more attractive to us than holding an unpredictable commodity. So, the next time someone asks whether gold belongs in your portfolio, our answer is simple: there are better ways to diversify, hedge inflation, and build long-term wealth—and they come with cashflows attached.